Duties and taxes on alcohol are a significant aspect of the beverage industry, impacting both producers and consumers worldwide. These levies, imposed by governments, vary widely depending on the type of alcohol, its alcohol content, and the country or region in question. Excise taxes, value-added taxes (VAT), and import duties are among the most common forms of taxation, with rates often designed to discourage excessive consumption, generate revenue for public services, or protect domestic industries. Understanding these duties and taxes is crucial for businesses navigating the alcohol market, as well as for consumers seeking to comprehend the final price of their favorite beverages.

Explore related products

What You'll Learn

![]()

Excise Duty Rates

In the European Union, excise duty rates on alcohol are harmonized to some extent but still allow member states flexibility in setting their own rates. The EU sets minimum excise duty rates for beer (€1.87 per hectoliter and degree Plato), wine (€0.00 per hectoliter for still wine, but member states can impose higher rates), and spirits (€0.785 per liter of pure alcohol). However, many countries exceed these minimums to generate revenue or discourage excessive consumption. For example, the United Kingdom imposes higher excise duties, with spirits taxed at £28.75 per liter of pure alcohol, beer at £19.08 per hectoliter, and wine at £2.23 per liter.

In India, excise duty rates on alcohol are determined at both the central and state levels, leading to significant variations across regions. The central government levies excise duty on spirits and beer, while states impose additional taxes on retail sales. For instance, the central excise duty on spirits is ₹150 per bulk liter, with additional taxes applied by states, often resulting in alcohol prices varying widely. Similarly, beer is taxed at ₹110 per bulk liter centrally, with state taxes further increasing the final price. These rates are periodically revised to align with fiscal policies and public health objectives.

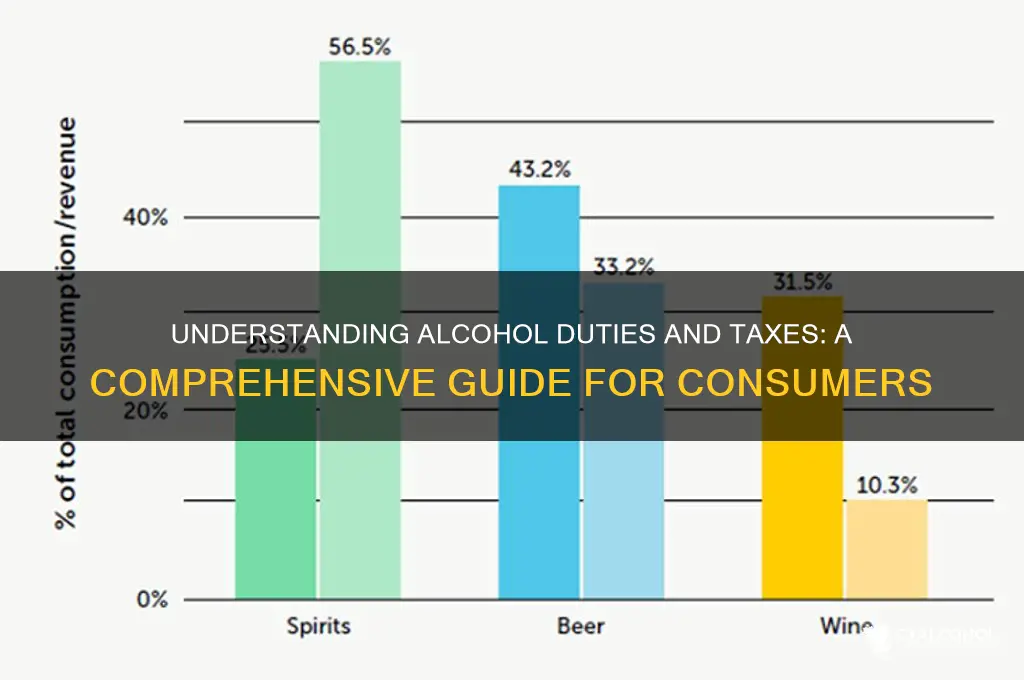

Australia employs a volumetric excise duty system for alcohol, where taxes are based on the volume of alcohol in a product rather than its price. The excise duty on spirits is $84.44 per liter of alcohol, while beer is taxed at $44.80 per liter of alcohol for products up to 3.5% ABV, and $67.20 per liter for stronger beers. Wine and other fermented beverages are subject to a Wine Equalisation Tax (WET) of 29% of the wholesale value, in addition to excise duty. This volumetric approach aims to create a fairer taxation system by focusing on alcohol content rather than product type.

Canada's excise duty rates on alcohol are set federally but vary by province due to additional provincial taxes. The federal excise duty on beer is $3.334 per hectoliter per degree Plato, while spirits are taxed at $13.864 per liter of absolute ethyl alcohol. Wine excise duties are lower, at $0.022 per liter, but provinces often impose markup fees and sales taxes, significantly increasing the final price. For example, in Ontario, the Liquor Control Board of Ontario (LCBO) adds additional charges, making alcohol prices among the highest in the country. These layered taxes highlight the complexity of excise duty structures in federal systems.

In summary, excise duty rates on alcohol are a critical component of taxation policies worldwide, designed to generate revenue, regulate consumption, and address public health concerns. The rates vary widely based on factors such as alcohol content, product type, and regional policies. Understanding these rates is essential for producers, distributors, and consumers, as they directly impact the cost and availability of alcoholic beverages. Whether through volumetric taxes, tiered structures, or harmonized minimums, excise duties play a pivotal role in shaping the alcohol market across different jurisdictions.

Alcohol Ice Packs: Safe or Not?

You may want to see also

Explore related products

![]()

Import Tariffs Explained

Import tariffs on alcohol are a critical component of the duties and taxes imposed on alcoholic beverages when they cross international borders. These tariffs are essentially taxes levied by governments on imported goods, including alcohol, and serve multiple purposes, such as protecting domestic industries, generating revenue, and regulating trade. For alcohol, import tariffs can vary significantly depending on the type of beverage (e.g., wine, beer, spirits), its alcohol content, and the country of origin. Understanding these tariffs is essential for importers, distributors, and even consumers, as they directly impact the final cost of the product.

The calculation of import tariffs on alcohol typically involves ad valorem taxes, which are based on the value of the imported goods, and specific taxes, which are levied per unit of alcohol (e.g., per liter or gallon). For instance, a country might impose a 10% ad valorem tariff on the customs value of imported wine, in addition to a specific excise tax of $2 per liter. These tariffs are often compounded with other duties, such as value-added tax (VAT) or sales tax, further increasing the cost of imported alcohol. The World Trade Organization (WTO) and regional trade agreements may influence these rates, but individual countries retain significant discretion in setting their tariff structures.

Import tariffs on alcohol are also influenced by bilateral and multilateral trade agreements. For example, countries within the European Union (EU) typically enjoy duty-free trade in alcohol among member states, while non-EU countries face higher tariffs. Similarly, the United States-Mexico-Canada Agreement (USMCA) outlines specific tariff reductions or exemptions for alcohol traded between these nations. However, countries outside such agreements often face higher tariffs, which can make their products less competitive in foreign markets. This dynamic underscores the importance of understanding the trade relationships between exporting and importing countries.

Compliance with import tariff regulations requires meticulous documentation and adherence to customs procedures. Importers must accurately declare the type, quantity, and value of the alcohol being imported, as well as provide proof of origin. Misdeclaration or non-compliance can result in penalties, seizure of goods, or legal action. Additionally, some countries impose labeling requirements, health warnings, or other standards that must be met before the alcohol can be cleared for sale. Navigating these requirements often necessitates the assistance of customs brokers or trade consultants.

Finally, import tariffs on alcohol have broader economic and social implications. High tariffs can protect domestic alcohol producers by making imported products more expensive, but they can also limit consumer choice and increase prices for end-users. Conversely, lower tariffs can foster competition, potentially driving down prices and encouraging innovation. Governments must balance these factors when setting tariff rates, considering both the interests of their domestic industries and the benefits of international trade. For businesses and consumers alike, staying informed about import tariffs is crucial for making strategic decisions in the global alcohol market.

Understanding the Scope of Addiction and Alcoholism in America

You may want to see also

Explore related products

![]()

Sales Tax Variations

The variation in sales tax rates becomes even more pronounced when considering local taxes. Many states allow local governments to impose additional sales taxes, which can further increase the price of alcohol. For example, in California, the state sales tax rate is 7.25%, but local taxes can add up to 2.5% more, resulting in a combined rate of 9.75% or higher in certain cities. This means that a bottle of wine or a case of beer can be significantly more expensive in one city compared to another within the same state. Understanding these local variations is essential for businesses to accurately price their products and for consumers to anticipate the final cost of their purchases.

Another critical aspect of sales tax variations is the distinction between different types of alcohol. Some states apply different tax rates for beer, wine, and spirits. For instance, in Illinois, the sales tax rate for beer and wine is the same as the general merchandise rate, but distilled spirits are subject to an additional tax. This tiered approach can make the tax structure more complex, requiring careful consideration when calculating the total tax liability. Additionally, some states may exempt certain types of alcohol from sales tax under specific conditions, such as for religious or medicinal purposes, further complicating the tax landscape.

Internationally, sales tax variations on alcohol are equally diverse. In the European Union, for example, Value Added Tax (VAT) rates on alcohol vary by country, with some applying reduced rates for specific types of beverages. The UK, post-Brexit, has its own VAT system, where alcohol is generally taxed at the standard rate of 20%, but certain exemptions or reduced rates may apply in specific circumstances. In contrast, countries like Canada have a Goods and Services Tax (GST) and Provincial Sales Tax (PST) or Harmonized Sales Tax (HST), depending on the province, which can significantly impact the final price of alcohol. These international variations highlight the importance of understanding local tax laws when dealing with alcohol sales across borders.

Lastly, it's important to consider how sales tax variations affect online alcohol sales and shipping. With the rise of e-commerce, many consumers purchase alcohol from out-of-state or international retailers. However, sales tax obligations can become complicated in these scenarios. Some states require online retailers to collect sales tax based on the buyer's location, while others may exempt certain transactions. Additionally, shipping alcohol across state lines may trigger additional taxes or fees, such as excise taxes or delivery fees, which are not always included in the initial purchase price. Navigating these complexities requires a thorough understanding of both the seller's and buyer's jurisdictions to ensure compliance and accurate pricing.

Alcohol Withdrawal Timeline: When Do Sweats Begin and What to Expect

You may want to see also

Explore related products

![]()

Licensing Fees Overview

Licensing fees are a critical component of the regulatory framework governing the alcohol industry, serving as a prerequisite for businesses to legally produce, distribute, or sell alcoholic beverages. These fees vary widely depending on the jurisdiction, type of license, and scale of operation. For instance, a small craft brewery may face different licensing costs compared to a large-scale distillery or a retail liquor store. The primary purpose of licensing fees is to fund regulatory oversight, ensure compliance with alcohol laws, and often contribute to public health and safety initiatives. Understanding these fees is essential for businesses to budget effectively and navigate the complex landscape of alcohol regulations.

In most regions, licensing fees are categorized based on the nature of the alcohol-related activity. For example, a manufacturer’s license for brewing beer, distilling spirits, or producing wine typically incurs higher fees due to the complexity of production and the need for stringent quality control. Similarly, wholesale and retail licenses come with their own fee structures, often tiered based on the volume of sales or the type of establishment. Bars, restaurants, and liquor stores, for instance, may face additional fees related to serving alcohol on-premises, which can include late-night operation permits or special event licenses. These fees are usually non-negotiable and must be renewed periodically, often annually, to maintain legal operation.

The calculation of licensing fees often takes into account factors such as the size of the business, its location, and the potential impact on the community. In some jurisdictions, fees may be higher in densely populated urban areas compared to rural regions, reflecting the greater regulatory burden and public health considerations. Additionally, businesses may be subject to surcharges or additional fees if they operate in areas with higher rates of alcohol-related incidents or if they seek specialized licenses, such as those for selling high-alcohol-content products. It is crucial for businesses to consult local regulatory bodies or legal experts to accurately determine their licensing fee obligations.

Another important aspect of licensing fees is their role in promoting responsible alcohol consumption and mitigating related societal issues. A portion of these fees often funds programs aimed at reducing drunk driving, underage drinking, and alcohol abuse. For example, some regions allocate licensing revenue to law enforcement agencies for increased patrols or to public health departments for education campaigns. This dual purpose of licensing fees—both regulatory and societal—highlights their significance beyond mere revenue generation for governments.

Finally, businesses must be aware of the potential for licensing fees to change over time due to legislative updates or shifts in public policy. Governments may adjust fees to address budget shortfalls, respond to public health crises, or align with new industry trends, such as the rise of craft alcohol production. Staying informed about these changes is vital to avoid penalties, license revocation, or disruptions to operations. Regularly reviewing updates from regulatory agencies and engaging with industry associations can help businesses stay compliant and plan for future fee adjustments. In summary, licensing fees are a multifaceted and dynamic aspect of the alcohol industry, requiring careful attention and strategic planning.

Understanding Alcoholism: A Guide for Sisters

You may want to see also

Explore related products

![]()

Customs Duties on Alcohol

The calculation of customs duties on alcohol is generally based on either the value of the goods (ad valorem duties) or a specific rate per unit of volume or alcohol content. Ad valorem duties are calculated as a percentage of the customs value, which includes the cost of the product, insurance, and freight. Specific duties, on the other hand, are fixed amounts applied per liter of alcohol or per liter of the product. Some countries use a combination of both methods to ensure a comprehensive taxation approach. For example, the European Union applies both ad valorem and specific duties on wine, spirits, and beer, with rates differing based on the product’s characteristics and origin.

In addition to customs duties, importers of alcohol often face other charges such as excise taxes, value-added tax (VAT), and additional fees related to health or environmental concerns. These charges are typically levied after customs duties and can significantly increase the final cost of the product. Excise taxes, in particular, are often applied at the point of importation and are based on the type and quantity of alcohol. VAT, which is common in many countries, is calculated as a percentage of the total cost, including customs duties and excise taxes, making the overall tax burden on alcohol substantial.

Compliance with customs duties on alcohol requires meticulous documentation and adherence to regulatory requirements. Importers must provide detailed invoices, certificates of origin, and other relevant documents to customs authorities. Failure to comply can result in delays, fines, or seizure of goods. Additionally, some countries have preferential trade agreements that reduce or eliminate customs duties for certain alcohol products originating from partner nations. Importers should leverage these agreements to optimize costs, but they must ensure eligibility and proper certification to benefit from reduced rates.

Understanding and managing customs duties on alcohol is essential for businesses involved in the international trade of alcoholic beverages. Given the complexity and variability of these duties, companies often consult customs brokers or trade experts to ensure accurate classification, valuation, and compliance. Staying informed about changes in regulations and trade policies is also crucial, as governments frequently update duty rates and rules to align with economic, health, or trade objectives. By proactively addressing customs duties, importers can minimize risks and maintain competitiveness in the global alcohol market.

Alcohol's Grip: When Dependency Takes Over

You may want to see also

Frequently asked questions

The main types of duties and taxes on alcohol include excise taxes, sales taxes, import duties, and value-added taxes (VAT). Excise taxes are levied based on the volume or type of alcohol, while sales taxes are applied at the point of purchase. Import duties are charged on alcohol brought into a country, and VAT is applied to the value of the product in some regions.

Excise taxes on alcohol are typically calculated based on the volume of alcohol (e.g., per liter of ethanol) or the type of beverage (e.g., beer, wine, spirits). Rates vary significantly by country and beverage type, with spirits often taxed at higher rates than beer or wine. Some jurisdictions also consider factors like alcohol content or packaging.

Yes, duties and taxes on alcohol often differ between domestic and imported products. Imported alcohol may face additional import duties and tariffs, while domestic products are subject to local excise taxes and sales taxes. These differences can impact the final price of alcohol, making imported products more expensive in some markets.