The Prohibition era in the United States, which lasted from 1919 to 1933, was preceded by a heavy tax burden on alcohol. Before the Prohibition, alcohol taxes contributed significantly to government revenue, accounting for 30 to 40 percent of the government's income. This revenue stream was crucial, reaching a peak of $310 million in 1866. The passage of the 16th Amendment in 1913, allowing for a federal income tax, paved the way for Prohibition by providing an alternative source of revenue. However, the implementation of Prohibition had unintended consequences, including a significant loss of tax revenue for the government, estimated at $11 billion, and the elimination of thousands of jobs related to the alcohol industry. The negative economic impact and the potential for the alcohol industry to generate revenue during the Great Depression contributed to the eventual repeal of Prohibition in 1933.

| Characteristics | Values |

|---|---|

| Prohibition period | 1919 to 1933 |

| Federal government's income from alcohol tax before Prohibition | 30% to 40% |

| Alcohol tax revenue in 1910 | $200 million |

| Amendment that allowed the federal government to levy income tax | 16th Amendment (1913) |

| Amendment that prohibited the manufacture, sale, and transportation of intoxicating beverages | 18th Amendment (1919) |

| Amendment that ended Prohibition | 21st Amendment (1933) |

| Act that legalised the sale of beer and wine with 3.2% alcohol content | Cullen-Harrison Act |

| Excise tax rates across states | $2.00 per gallon in Missouri, $36.55 per gallon in Washington |

| Excise tax rates across states (contd.) | Wyoming and New Hampshire have no excise taxes on spirits |

| Excise tax trends | Excise taxes have declined substantially in real terms since their inception |

| Excise tax trends (contd.) | Excise tax increases have become smaller over time for beer, distilled spirits, and wine |

Explore related products

What You'll Learn

- Alcohol excise taxes were a significant source of revenue for the government

- The 16th Amendment in 1913 allowed for a federal income tax

- Prohibitionists wanted to ban alcohol but needed to replace lost tax revenue

- Anti-German sentiment during WWI contributed to Prohibition

- The Great Depression caused a loss in income tax revenue, impacting Prohibition

![]()

Alcohol excise taxes were a significant source of revenue for the government

The passage of the 16th Amendment in 1913, which allowed for a national income tax, was a pivotal moment. This amendment paved the way for Prohibition by providing an alternative source of revenue for the government. With income tax in place, the government no longer relied solely on alcohol taxes, and the "loss of revenue question" that had plagued Prohibition advocates was resolved.

However, the impact of losing alcohol tax revenue was still significant. When Prohibition went into effect in 1920, it shut down the fifth-largest industry in the nation, resulting in thousands of job losses and a substantial loss of tax revenue for the government. The closing of breweries, distilleries, and saloons not only eliminated jobs in those industries but also had a ripple effect on related trades, such as barrel makers, truckers, and waiters.

The loss of tax revenue due to Prohibition continued to be a concern, especially as the nation entered the Great Depression in the 1930s. The potential to generate income and sales taxes from the alcohol industry, along with the creation of new jobs, contributed to the eventual repeal of Prohibition in 1933. The Cullen-Harrison Act, signed by President Franklin Delano Roosevelt, legalized the sale of low-alcohol beer and wine, bringing back the associated tax revenue.

While the specific rates and structures of alcohol excise taxes have evolved since the end of Prohibition, they continue to be a source of revenue for state and federal governments, with rates varying across different states.

How to Sneak Alcohol on a Plane Easily

You may want to see also

Explore related products

![]()

The 16th Amendment in 1913 allowed for a federal income tax

The 16th Amendment, ratified on February 3, 1913, established Congress's right to impose a federal income tax. The text of the amendment states:

> The Congress shall have the power to lay and collect taxes on incomes, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.

The 16th Amendment was proposed in 1909 by conservative Republicans who believed that an amendment would never be ratified by three-fourths of the states. However, the amendment was ratified by the required number of states on February 25, 1913, with the certification by Secretary of State Philander C. Knox.

The 16th Amendment had a significant impact on the way the federal government received funding. Before the amendment, the majority of funds given to the federal government came from tariffs on domestic and international goods, as well as taxes on alcohol, which accounted for 30 to 40% of the government's income. The new income tax amendment allowed the government to establish a nationwide income tax and reduce its reliance on alcohol taxes.

The passage of the 16th Amendment also had implications for Prohibition. With the ability to levy a national income tax, the government was no longer as dependent on revenue from alcohol taxes. This shift in taxation made it possible for the government to ban alcohol without facing a significant reduction in tax revenue.

Alcohol Detection: How Long Does it Last?

You may want to see also

Explore related products

![]()

Prohibitionists wanted to ban alcohol but needed to replace lost tax revenue

The Prohibition era in the United States began on January 19, 1920, and lasted until 1933. Before its implementation, there were questions about how the government would replace the revenue generated by alcohol taxes. Alcohol excise taxes were a significant source of income for the government, contributing around 30 to 40 percent of its revenue. By 1910, the federal government was collecting more than $200 million per year from the alcohol industry, second only to revenue from external trade tariffs.

The 16th Amendment, ratified in 1913, allowed the federal government to establish a nationwide income tax. This amendment was crucial in paving the way for Prohibition, as it provided a means to replace the lost revenue from alcohol taxes. The income tax lobby supported the Prohibition amendment in exchange for the enactment of the income tax amendment.

During the Prohibition era, the federal government lost a total of $11 billion in tax revenue and spent over $300 million on enforcement. The loss of revenue and the rise of the Great Depression in the 1930s shifted political will, as people questioned why they were foregoing tax revenue and jobs from alcohol sales and production.

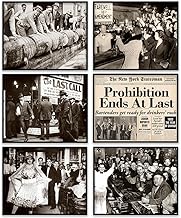

In 1932, Franklin Delano Roosevelt was elected President on a platform that included ending Prohibition. On March 22, 1933, he signed the Cullen-Harrison Act, legalizing the sale of beer and wine with an alcohol content of 3.2 percent, and the tax revenue associated with it. On December 5, 1933, the 21st Amendment was ratified, officially repealing Prohibition.

The impact of tax policy on Prohibition was significant, both in enabling the passage of the 18th Amendment and contributing to its eventual repeal. The implementation of income tax provided a solution to the "'loss of revenue' question" that had plagued Prohibitionists, allowing them to move forward with their mission of banning the sale of alcohol nationwide.

Alcohol-Related Hives: What You Need to Know

You may want to see also

Explore related products

![]()

Anti-German sentiment during WWI contributed to Prohibition

The United States' entry into World War I in 1917 brought with it a wave of anti-German sentiment. This was fuelled by increased anti-German propaganda for the war effort, which led to popular hysteria against German Americans. As a result, German Americans and their institutions came under attack, with businesses and homes vandalised and individuals accused of being "pro-German" tarred and feathered, and even lynched. This xenophobic rhetoric was also used against German-American brewers, who were vilified by temperance advocates.

By connecting alcohol production and consumption with German Americans, temperance advocates framed the issue as an "us vs. them" problem. This was effective because a large percentage of breweries were owned and operated by German Americans. Prohibitionists argued that money spent in brewers' pockets and grain diverted to breweries aided the German war effort. Posters connected the rationing of wheat with patriotism, implying that turning wheat into anything but bread was treasonous. This manipulation of anti-German sentiment was a powerful tool in the push for Prohibition.

The Food and Fuel Control Act of 1917, which outlawed the use of grains or foodstuffs for producing distilled spirits, further linked alcohol production to the war effort. This emergency wartime measure was set to expire at the end of World War I, but it prepared Americans for a future liquor ban. The war also shifted how the nation viewed itself, creating an opportunity for the prohibition movement to gain traction.

The Anti-Saloon League (ASL), led by Wayne Wheeler, was a powerful political pressure group that lobbied for the total prohibition of alcohol. Wheeler probed Congress to investigate organisations with ties to the Central Powers, specifically targeting the German-American Alliance. He revealed that the Busch family held German war bonds and even cared for wounded German soldiers, further associating alcohol production with support for Germany. This fed into the anti-German hysteria used by "drys" to gain support for Prohibition.

The Women's Christian Temperance Union (WCTU) and other progressive groups had been advocating for temperance and social reforms since the late 19th century. The war provided an opportunity to frame alcohol consumption as unpatriotic and a threat to the American war effort. With breweries accused of breaking up families and incapacitating American soldiers, the sentiment against alcohol became stronger, contributing to the eventual passage of the 18th Amendment in 1919, which prohibited the manufacture, sale, and transportation of intoxicating liquors.

Alcohol and Conception: What's the Connection?

You may want to see also

Explore related products

![]()

The Great Depression caused a loss in income tax revenue, impacting Prohibition

The United States' Prohibition era, which lasted from 1919 to 1933, was heavily influenced by tax policies and revenue concerns. Before the implementation of Prohibition, alcohol taxes were a significant source of income for the government, accounting for 30 to 40 percent of its revenue. This revenue stream was crucial in funding various government services and activities.

However, the passage of the 16th Amendment in 1913, which allowed the federal government to levy a national income tax, changed the landscape. This amendment provided an alternative source of revenue, paving the way for the 18th Amendment and the subsequent Prohibition. With the income tax in place, the government no longer relied solely on alcohol taxes, and the movement to ban alcohol gained momentum, driven by groups like the Anti-Saloon League.

During the Prohibition era, the unintended consequences became apparent. The closure of breweries, distilleries, and saloons resulted in significant job losses, impacting various related trades. Additionally, the federal government faced a substantial loss in tax revenue, amounting to $11 billion during Prohibition. The stock market crash of 1929 and the ensuing Great Depression further exacerbated the situation, causing a decline in income tax revenues.

As the nation struggled with the economic fallout of the Great Depression, the potential for the alcohol industry to generate new jobs and boost tax revenues through sales and production became increasingly appealing. The loss in income tax revenue during this period highlighted the opportunity costs of maintaining Prohibition. This shift in perspective, combined with the economic crisis, played a significant role in shaping political will and ultimately contributed to the end of Prohibition.

In 1932, Franklin Delano Roosevelt was elected President, and the tide began to turn. On March 22, 1933, Roosevelt signed the Cullen-Harrison Act, legalizing the sale of beer and wine with low alcohol content and marking a pivotal moment in the resurrection of the alcohol tax base. Just nine months later, in December 1933, the 21st Amendment was ratified, bringing an end to Prohibition nationwide.

Whiskey Wisdom: How Much Alcohol in a Shot?

You may want to see also

Frequently asked questions

Between 30 to 40 percent of the government's income came from taxes on liquor, wine, and beer.

No, in the early days of the colonies, they were exempt from nearly all taxes except some import duties and an annual land tax.

The 16th Amendment, ratified in 1913.

Yes, when Prohibition went into effect in 1920, the government lost out on a significant source of revenue.

Yes, when Prohibition was repealed in 1933, alcohol taxes were reintroduced, with the income tax working alongside the liquor tax to generate revenue.