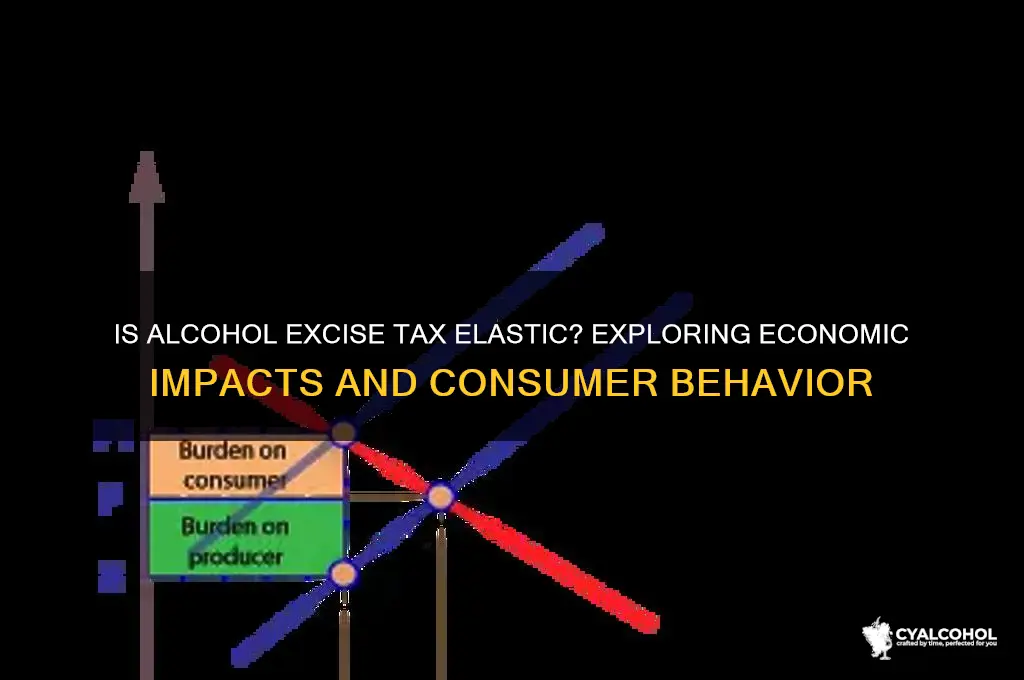

The concept of whether alcohol is elastic in relation to excise tax is a critical economic question that explores how changes in alcohol taxation impact consumer behavior and market dynamics. Elasticity refers to the degree to which demand for a product responds to price changes; if alcohol demand is elastic, a tax increase would significantly reduce consumption, while inelastic demand suggests minimal impact. Excise taxes on alcohol are commonly used by governments to generate revenue and address public health concerns, such as reducing excessive drinking and related societal costs. Understanding the elasticity of alcohol demand is essential for policymakers to balance fiscal goals with public health objectives, as it determines the effectiveness of tax measures in curbing consumption and their potential revenue implications.

Explore related products

What You'll Learn

![]()

Impact on Consumer Behavior

Alcohol excise taxes significantly influence consumer behavior, particularly in how individuals allocate their spending and choose beverages. When taxes increase, consumers often respond by reducing their overall alcohol consumption or shifting to cheaper alternatives. For instance, a 10% increase in beer taxes has been shown to decrease beer consumption by 5-7% among adults aged 21-30, a demographic highly sensitive to price changes. This elasticity highlights how younger consumers, often with tighter budgets, are more likely to adjust their drinking habits in response to higher costs.

Consider the practical implications for households. A family that spends $50 weekly on alcohol might cut back to $35 if taxes rise, opting for store brands over premium labels or reducing the frequency of purchases. This behavior is not limited to low-income groups; even middle-income consumers tend to trade down to more affordable options. For example, a shift from craft beer to domestic brands or from imported wine to local varieties is common. Retailers often observe a 12-15% increase in sales of lower-priced alcohol categories within six months of a tax hike, underscoring this adaptive behavior.

From a health perspective, excise taxes can inadvertently promote moderation. Studies indicate that a 1% increase in alcohol prices correlates with a 0.5% reduction in alcohol-related hospitalizations among individuals aged 40-60. While not all consumers reduce intake, those with higher health risks or pre-existing conditions are more likely to respond positively. Public health campaigns can amplify this effect by educating consumers about the financial and health benefits of cutting back, especially when paired with tax increases.

However, the impact isn’t uniform across all demographics or beverage types. Spirits, for example, exhibit lower price elasticity compared to beer or wine, as consumers perceive them as luxury items. Wealthier individuals aged 35-55 are less likely to alter their consumption patterns, even with substantial tax increases. Conversely, younger and lower-income groups show greater sensitivity, often substituting alcohol with non-alcoholic beverages or social activities. Policymakers must consider these disparities to avoid disproportionately affecting vulnerable populations.

To navigate these changes, consumers can adopt strategies like bulk purchasing during sales, exploring loyalty programs, or diversifying their beverage choices to include lower-taxed options. For instance, in regions where wine taxes are lower than spirits, consumers might opt for wine-based cocktails instead of traditional liquor-based drinks. Understanding local tax structures and planning purchases accordingly can mitigate the financial impact while maintaining social and recreational habits. Ultimately, the elasticity of alcohol excise taxes serves as both a financial and behavioral lever, shaping not just spending but also consumption patterns across diverse consumer groups.

Understanding DUI/DWI Charges: What Does or Any Similar Alcohol Offense Mean?

You may want to see also

Explore related products

![]()

Revenue Generation for Governments

Alcohol excise taxes are a critical revenue stream for governments worldwide, but their effectiveness hinges on understanding the elasticity of alcohol demand. Elasticity measures how sensitive consumption is to price changes. If alcohol demand is highly elastic, a tax increase will significantly reduce consumption, potentially limiting revenue gains. Conversely, inelastic demand means consumers will continue buying despite higher prices, ensuring steady or increased tax revenue. For instance, studies show that beer demand tends to be more elastic among younger consumers (ages 18–25) compared to older demographics, who may be less sensitive to price hikes. This variability underscores the need for governments to tailor tax policies based on age groups and beverage types to maximize revenue without overly burdening specific populations.

To optimize revenue generation, governments must balance tax rates with public health goals. A well-designed excise tax can discourage excessive consumption while generating funds for healthcare, education, or infrastructure. For example, a 10% increase in alcohol taxes has been shown to reduce consumption by 5–7% in countries with moderate drinking cultures, such as Canada and Australia. However, in regions with high alcohol dependency, such as Eastern Europe, the same increase might yield only a 2–3% reduction in consumption, highlighting the importance of regional context. Governments can enhance revenue predictability by implementing tiered tax structures, where higher-alcohol beverages (e.g., spirits) are taxed at higher rates than lower-alcohol options (e.g., beer), encouraging consumers to shift to less harmful choices while maintaining tax income.

A practical strategy for governments is to index alcohol excise taxes to inflation or income levels, ensuring they remain effective over time. Without regular adjustments, real tax rates erode, reducing both revenue and public health benefits. For instance, the United Kingdom’s alcohol duty system, which is reviewed annually, has successfully maintained revenue stability while adapting to economic changes. Additionally, governments can introduce minimum unit pricing (MUP) to target cheap, high-strength products often associated with harmful consumption. Scotland’s MUP policy, set at 50 pence per unit of alcohol, reduced alcohol-related hospital admissions by 13% within three years, demonstrating how targeted measures can improve public health without sacrificing revenue.

Finally, transparency and communication are essential for public acceptance of alcohol excise taxes. Governments should clearly articulate how tax revenues are allocated, such as funding addiction treatment programs or subsidizing public transportation. For example, Norway’s alcohol tax revenues are partially directed to youth sports initiatives, fostering public support for the policy. Pairing tax increases with public awareness campaigns about the health risks of alcohol can further legitimize these measures. By combining economic strategy with social responsibility, governments can ensure alcohol excise taxes remain a sustainable and effective tool for revenue generation.

Alcohol and Metronidazole: Dangerous Interactions You Need to Avoid

You may want to see also

Explore related products

![]()

Elasticity in Alcohol Demand

Alcohol demand elasticity measures how sensitive consumption is to price changes, a critical factor when evaluating the impact of excise taxes. For instance, a 10% increase in alcohol prices typically reduces consumption by 4-8%, depending on the beverage type and demographic. This responsiveness varies: beer demand tends to be more elastic than spirits, as consumers often view beer as a discretionary purchase. Younger adults (ages 21-34) exhibit higher elasticity, likely due to tighter budgets and greater price sensitivity, while older demographics show more inelastic demand, prioritizing habit over cost.

Consider the practical implications for policymakers. Excise taxes on alcohol can reduce consumption, but their effectiveness hinges on understanding elasticity. For example, a $0.25 tax increase on a six-pack of beer might deter college students more than a $2 tax increase on a bottle of whiskey would deter affluent professionals. To maximize public health benefits, taxes should target beverages with higher elasticity, such as beer and wine, while accounting for regional drinking patterns. For instance, in areas with high beer consumption, even modest tax hikes could yield significant reductions in binge drinking.

From a consumer perspective, elasticity influences purchasing decisions. Budget-conscious drinkers may switch to cheaper brands or reduce quantity when prices rise, while brand-loyal consumers might absorb the cost. For example, a craft beer enthusiast might cut back from 12 to 6 weekly purchases if prices increase by 15%, whereas a casual wine drinker might opt for store brands instead of premium labels. Retailers can leverage this by offering discounts on elastic products during tax hikes to maintain sales volume.

Comparatively, alcohol’s elasticity contrasts with that of necessities like food or healthcare, which are typically inelastic. Unlike insulin or bread, alcohol is discretionary, making its demand more responsive to price. However, within the alcohol category, elasticity varies by income level. Low-income households exhibit higher elasticity, often reducing consumption sharply when prices rise, while high-income households may barely notice the change. This disparity underscores the regressive nature of alcohol excise taxes, disproportionately affecting those least able to pay.

In conclusion, understanding elasticity in alcohol demand is essential for crafting effective tax policies and consumer strategies. Policymakers can use elasticity data to design taxes that reduce harmful consumption without overly burdening specific groups. Consumers and retailers can navigate price changes by prioritizing value and flexibility. For instance, a family planning a party might opt for bulk purchases of elastic beverages like beer during tax-free periods, while a bar owner could introduce happy hour specials to offset tax-induced price increases. By focusing on elasticity, stakeholders can balance public health goals with economic realities.

Safe Drinking: Units and You

You may want to see also

Explore related products

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UY218_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UY218_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UY218_.jpg)

![]()

Tax Policy and Public Health

Alcohol excise taxes are a powerful tool for shaping public health outcomes, but their effectiveness hinges on understanding the elasticity of alcohol demand. Elasticity measures how sensitive consumption is to price changes. When alcohol demand is highly elastic, even modest tax increases can significantly reduce consumption, particularly among price-sensitive groups like youth and heavy drinkers. For instance, a 10% increase in alcohol prices has been associated with a 5-7% decrease in overall consumption, according to the World Health Organization. This relationship underscores the potential of tax policy to mitigate alcohol-related harms, including liver disease, injuries, and social costs.

To maximize public health benefits, policymakers must consider the design of excise taxes. Ad valorem taxes, which are based on the value of the product, may become less effective over time due to inflation. In contrast, specific excise taxes, which are fixed amounts per unit of alcohol, maintain their real value and provide a more consistent deterrent to consumption. For example, countries like Ireland and Scotland have implemented minimum unit pricing (MUP) policies, effectively setting a floor price for alcohol. This approach targets cheap, high-strength beverages often favored by harmful drinkers, reducing consumption without disproportionately affecting moderate users.

However, the success of alcohol taxation in improving public health requires careful implementation and monitoring. Tax increases must be substantial enough to influence behavior but not so high as to encourage illicit trade or tax evasion. Evidence from Mexico suggests that a 20% increase in the excise tax on sugar-sweetened beverages led to a 12% reduction in purchases, demonstrating the potential for similar impacts on alcohol. Additionally, revenue generated from these taxes should ideally be reinvested in public health initiatives, such as addiction treatment programs or awareness campaigns, to amplify their benefits.

A critical aspect of tax policy is its equity implications. While higher taxes can reduce consumption, they may also place a greater financial burden on low-income individuals who spend a larger proportion of their income on alcohol. To address this, policymakers can pair tax increases with targeted subsidies or social programs that support vulnerable populations. For example, Canada’s excise tax on alcohol includes exemptions for small producers, balancing public health goals with economic considerations. Such nuanced approaches ensure that tax policies are both effective and fair.

Ultimately, the intersection of tax policy and public health offers a compelling case for using alcohol excise taxes as a preventive measure. By leveraging elasticity principles and adopting evidence-based strategies, governments can reduce alcohol-related harms while generating revenue for health initiatives. Practical steps include indexing taxes to inflation, implementing minimum unit pricing, and reinvesting tax revenue in community health programs. When designed thoughtfully, alcohol taxation becomes more than a fiscal tool—it becomes a lifeline for public health.

Alcohol's Macronutrient Mystery: Carbohydrate, Fat, or Something Else?

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [PC/Mac Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [PC Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![]()

Industry Response to Excise Taxes

Excise taxes on alcohol, often levied to curb consumption and generate revenue, prompt varied and strategic responses from the industry. One common tactic is price optimization, where producers adjust pricing to offset tax increases without alienating consumers. For instance, a 10% excise tax hike might lead to a 5% price increase, with the remaining 5% absorbed by reducing profit margins or cutting operational costs. This approach leverages the elasticity of alcohol demand, where premium brands may retain loyal customers despite higher prices, while budget options risk losing price-sensitive buyers.

Another industry response is product innovation, particularly in developing lower-alcohol or alcohol-free alternatives. Companies like Heineken and AB InBev have expanded their portfolios to include 0.0% beer options, targeting health-conscious consumers while diversifying revenue streams. This strategy not only mitigates the impact of excise taxes but also aligns with shifting consumer preferences for moderation. For example, in countries with tiered excise taxes based on alcohol content, a 4% ABV beer might face a 20% lower tax rate than its 5% counterpart, incentivizing such innovations.

Lobbying and advocacy also play a critical role in shaping excise tax policies. Industry associations, such as the Distilled Spirits Council in the U.S., often argue that excessive taxes harm small businesses and reduce employment. They may propose alternative revenue measures, like increasing sales taxes, which are perceived as less burdensome on specific sectors. In 2021, the U.S. alcohol industry successfully lobbied for a temporary reduction in excise taxes under the Craft Beverage Modernization and Tax Reform Act, highlighting the effectiveness of collective action.

Finally, marketing and consumer education are employed to maintain brand loyalty in the face of tax-driven price increases. Campaigns emphasizing quality, heritage, or unique production methods can justify higher prices, as seen with craft breweries and distilleries. For instance, a small-batch whiskey producer might highlight its 12-year aging process to differentiate itself from mass-market competitors, allowing it to pass on excise tax costs without losing market share.

In summary, the alcohol industry responds to excise taxes through a combination of price optimization, product innovation, lobbying, and strategic marketing. Each approach reflects an understanding of consumer behavior, regulatory landscapes, and market dynamics, ensuring resilience in a taxed environment.

Is Stearyl Alcohol Water-Soluble? Exploring Its Solubility Properties

You may want to see also

Frequently asked questions

An elastic alcohol excise tax means that changes in the tax rate significantly affect the demand for alcohol. When the tax increases, consumers reduce their purchases more substantially, and when the tax decreases, consumption rises noticeably.

If alcohol excise tax is elastic, raising the tax rate may not always increase government revenue. Since higher taxes lead to a larger drop in consumption, the additional revenue from the higher tax rate may be offset by the reduced quantity sold.

Alcohol excise tax is often more elastic because alcohol is a non-essential good, and consumers can easily reduce or substitute their consumption in response to price changes. Additionally, the availability of alternatives (e.g., non-alcoholic beverages) makes demand more sensitive to tax increases.

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)