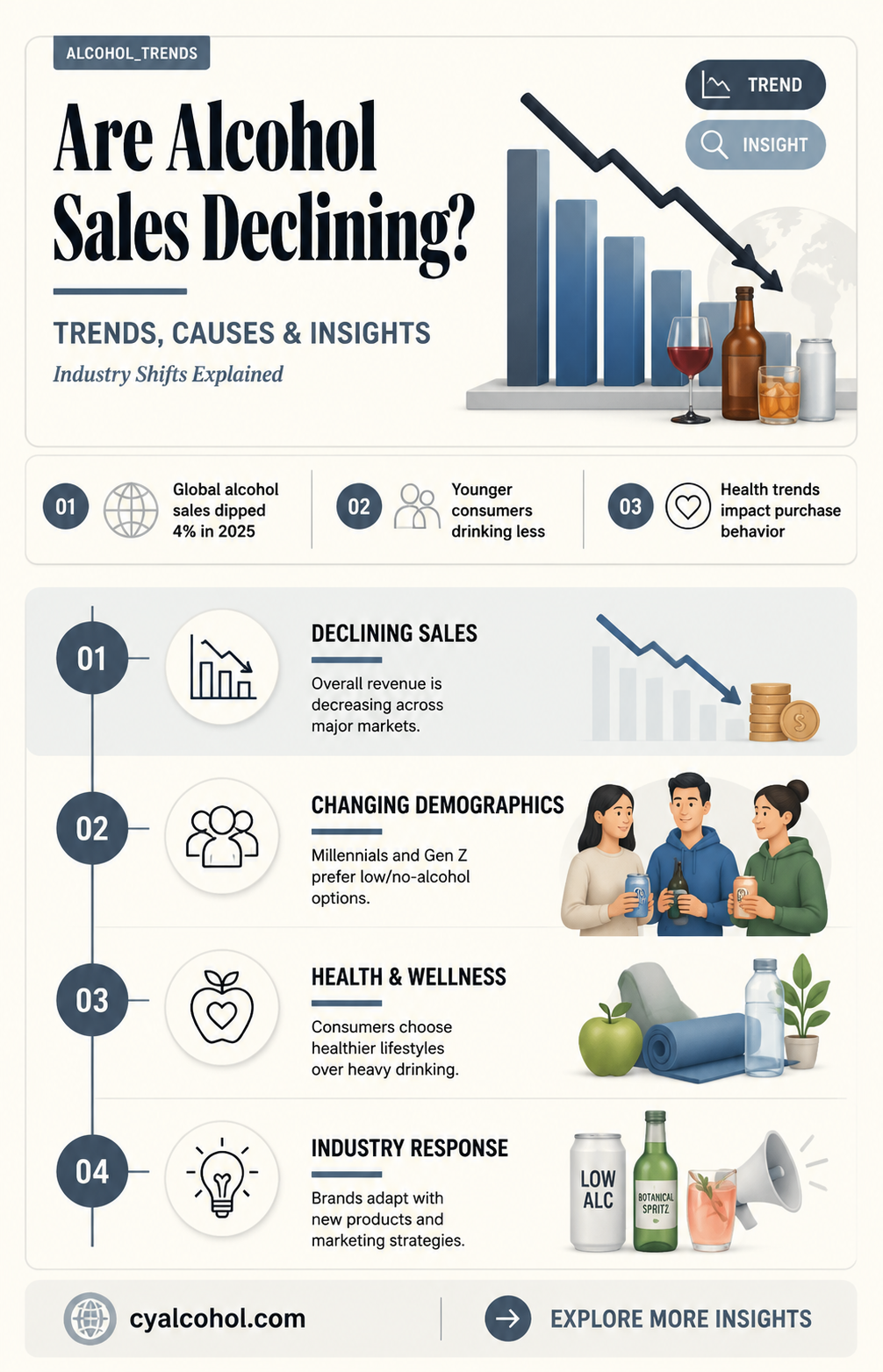

Recent data and industry reports suggest that alcohol sales may be experiencing a decline in certain markets, prompting questions about the factors driving this trend. Economic shifts, changing consumer preferences, and the rise of health-conscious lifestyles are among the key contributors to this potential downturn. Additionally, the growth of non-alcoholic alternatives and the impact of the COVID-19 pandemic on drinking habits have further influenced the landscape. As businesses and analysts examine these developments, understanding the underlying causes and implications for the alcohol industry becomes increasingly important.

| Characteristics | Values |

|---|---|

| Overall Trend (2023) | Mixed. Some reports indicate a slight decline, while others show stability or modest growth compared to pre-pandemic levels. |

| Key Drivers of Decline | - Economic Factors: Inflation, rising costs of living, and economic uncertainty leading to reduced discretionary spending. - Health Consciousness: Growing awareness of health risks associated with alcohol consumption, leading to moderation or abstinence. - Changing Consumer Preferences: Shift towards non-alcoholic beverages, low-alcohol options, and craft/premium products. < - E-commerce Impact: Online sales disrupting traditional retail channels, potentially impacting overall sales figures. |

| Regional Variations | - North America: Sales largely stable or slightly declining. - Europe: Mixed trends, with some countries experiencing declines while others remain stable. - Asia-Pacific: Growth in some markets, particularly for premium and craft beverages, but overall growth slowing. |

| Product Categories | - Beer: Sales declining in some regions, particularly mass-market brands, while craft and specialty beers show resilience. - Wine: Stable or slightly declining, with a shift towards premium and organic options. - Spirits: Mixed trends, with some categories (e.g., whiskey, tequila) experiencing growth while others decline. |

| Future Outlook | Uncertain. Factors like economic recovery, changing consumer habits, and industry innovation will influence future trends. |

Explore related products

$25.36 $25.36

What You'll Learn

![]()

Impact of COVID-19 lockdowns on alcohol sales trends

The COVID-19 lockdowns disrupted alcohol sales in unprecedented ways, shifting consumer behavior and industry dynamics. Initially, panic buying led to a surge in off-premise sales, with Nielsen reporting a 54% increase in alcohol sales during the first week of lockdowns in March 2020. Supermarkets and liquor stores saw shelves emptied as consumers stocked up on wine, beer, and spirits, anticipating prolonged confinement. This spike, however, was short-lived, giving way to more nuanced trends as the lockdowns persisted.

As weeks turned into months, the nature of alcohol consumption changed dramatically. With bars, restaurants, and social gatherings shut down, on-premise sales plummeted by over 80% in some regions, according to IWSR Drinks Market Analysis. This forced a rapid pivot in the industry, with many establishments offering takeout cocktails and delivery services to stay afloat. Meanwhile, off-premise sales continued to rise, but at a slower pace, as consumers settled into new routines. Virtual happy hours and at-home mixology became popular, driving demand for premium spirits and craft beers, while cheaper, bulk options also gained traction due to economic uncertainty.

The lockdowns also highlighted disparities in alcohol sales across demographics. Younger consumers, particularly those aged 21–34, reduced their alcohol intake, with a 2020 survey by Morning Consult showing a 17% decrease in this age group. This was attributed to factors like financial strain, reduced social opportunities, and a focus on health during the pandemic. Conversely, older demographics, especially those aged 55 and above, maintained or slightly increased their consumption, often opting for wine and spirits. These shifts underscored the importance of targeted marketing strategies to address varying consumer needs.

A notable trend was the rise of e-commerce in alcohol sales, which grew by 243% in 2020, according to Drizly. Brands that had previously relied on traditional retail channels were forced to invest in online platforms, partnerships with delivery apps, and direct-to-consumer models. This digital transformation is likely to outlast the pandemic, as consumers appreciate the convenience of home delivery. However, regulatory hurdles, such as state-specific alcohol laws in the U.S., remain a challenge for widespread adoption.

In conclusion, the COVID-19 lockdowns reshaped alcohol sales trends in ways that will have lasting implications. While off-premise sales and e-commerce experienced significant growth, on-premise sales suffered, and consumer preferences became more polarized. Understanding these shifts is crucial for businesses to adapt and thrive in a post-pandemic world. Practical tips for retailers include diversifying product offerings to cater to both premium and budget-conscious consumers, investing in digital infrastructure, and leveraging data analytics to identify emerging trends.

Foods That Slow Alcohol Absorption: Smart Snacks for Safer Drinking

You may want to see also

Explore related products

$13.6 $17.99

![]()

Shift to at-home drinking vs. bars and restaurants

The pandemic accelerated a trend already bubbling under the surface: more people are opting for at-home drinking over bars and restaurants. This shift isn’t just about convenience; it’s a cultural pivot reshaping how alcohol is consumed, marketed, and even packaged. Data from Nielsen shows that off-premise alcohol sales (stores, online) surged by 27% in 2020, while on-premise sales (bars, restaurants) plummeted by 23%. This disparity highlights a clear consumer preference for the comfort and control of home drinking.

Consider the practicalities: at-home drinking allows for precise budgeting. A bottle of wine at a restaurant can cost three times its retail price, whereas a $15 bottle from a store can serve multiple occasions. For those tracking intake, home drinking offers transparency—you know exactly how much you’re pouring. For instance, a standard drink is 5 ounces of wine (12% ABV), 12 ounces of beer (5% ABV), or 1.5 ounces of spirits (40% ABV). At home, measuring these portions is straightforward, whereas in a bar, portion sizes can vary wildly.

However, the shift isn’t without its downsides. Bars and restaurants thrive on social interaction, and their decline impacts not just the economy but also communal drinking culture. The ritual of meeting friends for a drink, the ambiance of a dimly lit bar, or the expertise of a mixologist—these experiences are hard to replicate at home. To bridge this gap, some consumers are investing in home bars, cocktail kits, and virtual tastings. For example, sales of cocktail shakers and bartending tools rose by 40% in 2021, according to market research firm NPD Group.

From a marketing perspective, brands are adapting by targeting the home consumer. Mini bottles, single-serve cans, and ready-to-drink cocktails are booming. Hard seltzers, for instance, saw a 150% sales increase in 2020, largely due to their convenience and lower alcohol content (typically 4-6% ABV), appealing to health-conscious drinkers. Even wine brands are offering smaller formats, like 500ml bottles, perfect for solo evenings or paired dinners.

The takeaway? At-home drinking is here to stay, but it’s evolving. Consumers want the best of both worlds: the affordability and control of home drinking, paired with the sophistication and social elements of bars. For those navigating this shift, the key is balance—curate your home setup with quality tools, experiment with recipes, and occasionally splurge on a night out to keep the bar scene alive. After all, while home drinking may be convenient, there’s no substitute for the clink of glasses with friends.

Yeast Alcoholic Fermentation: Does It Produce Glucose?

You may want to see also

Explore related products

![]()

Rise of non-alcoholic beverage alternatives

Alcohol sales have been on a downward trajectory in recent years, and one of the most significant contributors to this trend is the surge in popularity of non-alcoholic beverage alternatives. This shift is not merely a fad but a reflection of changing consumer preferences, driven by health consciousness, lifestyle choices, and innovative product offerings. For instance, in 2023, the global non-alcoholic beverage market grew by 8%, outpacing the alcoholic beverage sector, which saw a 2% decline. This data underscores a broader cultural movement toward moderation and wellness.

Analyzing the rise of non-alcoholic options reveals a strategic response to consumer demands. Brands like Athletic Brewing and Seedlip have pioneered the market by offering sophisticated, alcohol-free alternatives that mimic the complexity of traditional drinks. For example, Seedlip’s botanical blends provide a gin-like experience without the alcohol, appealing to those who enjoy the ritual of mixing cocktails but prefer to avoid intoxication. Similarly, non-alcoholic beers now account for 3% of total beer sales in the U.S., with options like Heineken 0.0 gaining traction among health-conscious consumers and designated drivers.

From a practical standpoint, incorporating non-alcoholic beverages into daily routines is easier than ever. For those looking to reduce alcohol intake, experts recommend starting with a 1:1 replacement strategy—swap one alcoholic drink for a non-alcoholic alternative at social gatherings. For instance, a non-alcoholic wine like Surely can pair seamlessly with dinner, offering the same sensory experience without the alcohol content. Additionally, younger demographics, particularly millennials and Gen Z, are driving this trend, with 40% reporting they drink less alcohol than previous generations, often opting for mocktails or zero-proof spirits instead.

The health benefits of choosing non-alcoholic alternatives are compelling. Studies show that reducing alcohol consumption can improve sleep quality, enhance liver function, and lower the risk of chronic diseases. For example, cutting out alcohol can reduce daily calorie intake by 200-500 calories, aiding in weight management. Moreover, non-alcoholic beverages often contain functional ingredients like adaptogens or vitamins, further aligning with wellness trends. A 2022 survey found that 65% of consumers choose non-alcoholic options for their perceived health benefits, highlighting the intersection of taste and nutrition.

In conclusion, the rise of non-alcoholic beverage alternatives is not just a reaction to declining alcohol sales but a proactive movement toward healthier, more mindful consumption. With innovative products, strategic marketing, and a clear focus on consumer needs, this sector is reshaping the beverage industry. Whether you’re looking to cut back on alcohol or simply explore new flavors, non-alcoholic options offer a versatile and satisfying solution. As the market continues to evolve, one thing is clear: the future of beverages is inclusive, health-focused, and deliciously diverse.

Unveiling the Mystery: What is Alcohol Whistlindiesel and How It Works

You may want to see also

Explore related products

![]()

Economic factors affecting consumer spending on alcohol

Recent data reveals a noticeable dip in alcohol sales, prompting a closer examination of the economic forces at play. One significant factor is the inflationary pressure on disposable income. As the cost of living rises, consumers are forced to reallocate their budgets, often cutting back on non-essential items like alcohol. For instance, a 2023 report by NielsenIQ highlighted that 45% of consumers in the U.S. reduced their spending on alcoholic beverages due to financial constraints. This trend is particularly pronounced among younger demographics, such as millennials and Gen Z, who are more likely to prioritize essentials like rent and groceries over discretionary purchases.

Another critical economic factor is the shift in consumer behavior driven by recession fears. During periods of economic uncertainty, households tend to adopt a more conservative spending mindset. Alcohol, especially premium and craft varieties, is often the first to be sacrificed in favor of cheaper alternatives or abstinence. For example, sales of high-end wines and spirits have declined by 8% year-over-year, while budget-friendly options like boxed wine and domestic beer have seen modest growth. This shift underscores the elasticity of demand for alcohol, which is highly sensitive to changes in consumer confidence and economic stability.

The impact of taxation and regulatory policies cannot be overlooked either. Governments worldwide have implemented higher taxes on alcohol to curb consumption and generate revenue, further dampening sales. In the UK, for instance, the 2022 alcohol duty reforms led to a 10% increase in prices, resulting in a 6% drop in sales volume within the first quarter. Similarly, countries like Ireland and Scotland have introduced minimum unit pricing, making alcohol less affordable for price-sensitive consumers. These policies not only reduce overall consumption but also push consumers toward lower-priced or untaxed alternatives, such as home-brewed beverages or non-alcoholic drinks.

Lastly, the rise of health-conscious consumerism intersects with economic factors to influence alcohol spending. As awareness of the health and financial costs of alcohol grows, many are opting to reduce or eliminate their intake. This trend is particularly evident among the 25-40 age group, where 30% report cutting back on alcohol for health reasons. Economically, this shift aligns with the desire to save money, as the average household can save up to $500 annually by reducing alcohol consumption. Non-alcoholic beverages, which are often cheaper and perceived as healthier, have seen a 35% increase in sales, further diverting spending away from traditional alcohol markets.

In summary, economic factors such as inflation, recession fears, taxation, and shifting consumer priorities are collectively driving the decline in alcohol sales. Understanding these dynamics is crucial for both consumers and industry stakeholders, as it highlights the need for adaptability in a changing economic landscape. For consumers, prioritizing financial health and exploring cost-effective alternatives can mitigate the impact of these trends. For businesses, innovating with affordable products and catering to health-conscious demands may be key to weathering the downturn.

Alcohol and Heart Health: Does Drinking Raise Heart Attack Risk?

You may want to see also

Explore related products

![]()

Changing health and wellness trends reducing alcohol consumption

Alcohol sales are declining, and a significant driver is the growing emphasis on health and wellness. Consumers are increasingly aware of the detrimental effects of alcohol, from its caloric content to its impact on mental health and long-term disease risk. This shift is evident in the rise of sober-curious movements, where individuals reduce or eliminate alcohol without identifying as abstinent. For instance, a 2023 Nielsen report highlights that 66% of global consumers are willing to pay more for products that support their health goals, including non-alcoholic beverages. This trend is reshaping the market, with brands like Athletic Brewing and Seedlip capitalizing on the demand for sophisticated, alcohol-free alternatives.

Consider the caloric impact of alcohol: a single glass of wine (5 ounces) contains approximately 120 calories, while a pint of beer averages 150 calories. Over time, these calories add up, contributing to weight gain and metabolic issues. Health-conscious consumers are now opting for zero-calorie or low-calorie alternatives, such as sparkling water with a splash of fruit juice or kombucha, which offers probiotics and fewer than 50 calories per serving. This shift is not just about weight management but also about overall well-being, as excessive alcohol consumption is linked to liver disease, cardiovascular problems, and impaired cognitive function.

The wellness industry’s focus on mental health has also played a pivotal role in reducing alcohol consumption. Studies show that even moderate drinking can exacerbate anxiety and depression, particularly in younger adults aged 18–34. This demographic is increasingly turning to mindfulness practices, meditation apps, and fitness routines as healthier ways to manage stress. For example, platforms like Headspace and Peloton have seen exponential growth, offering alcohol-free ways to unwind. Practical tips for replacing evening drinks include brewing herbal tea (e.g., chamomile for relaxation) or engaging in a 20-minute yoga session to reduce cortisol levels.

Comparatively, the alcohol industry is responding with innovation, but it’s an uphill battle. While low-alcohol and non-alcoholic beers now account for 3% of the beer market, traditional sales continue to decline. The challenge lies in overcoming the cultural association of alcohol with socializing. However, health-focused events like sober brunches, mocktail nights, and fitness-oriented meetups are gaining popularity, offering alternatives that prioritize connection without alcohol. For those transitioning, experts recommend setting clear boundaries, such as limiting drinking to weekends or choosing non-alcoholic options at social gatherings, to maintain progress without feeling deprived.

In conclusion, the decline in alcohol sales is deeply intertwined with the health and wellness movement. Consumers are making informed choices, prioritizing long-term well-being over temporary indulgence. Whether through calorie-conscious decisions, mental health awareness, or cultural shifts, this trend is reshaping both individual habits and the beverage industry. For those looking to reduce alcohol intake, combining education, practical alternatives, and community support can make the transition seamless and sustainable.

Alcohol's Impact on Youth: Risks, Effects, and Long-Term Consequences

You may want to see also

Frequently asked questions

Alcohol sales have experienced fluctuations, with some regions and categories showing declines, particularly in traditional beer and spirits. However, overall sales remain strong, driven by growth in premium and craft segments.

Factors include changing consumer preferences toward health and wellness, increased competition from non-alcoholic beverages, economic pressures, and shifting demographics, especially among younger consumers.

Not all categories are declining. Ready-to-drink cocktails, hard seltzers, and low-alcohol beverages are growing, while traditional beer and spirits face challenges. Wine sales remain relatively stable.

Companies are innovating with new products like non-alcoholic and low-calorie options, expanding into premium and craft markets, and leveraging marketing strategies to appeal to health-conscious and younger consumers.